So, you just earned the bonus on your Chase Sapphire Preferred® Card. But, what’s next?

By signing up for your next card, you’ll maximize your rewards and earn even more cash back.

With your new Chase Sapphire card in your wallet, you’ll want to keep the momentum going by earning more rewards. We’ve made this simple and easy for you to find the next best card to maximize your overall cash back opportunities.

Don’t let this information overwhelm you—you’ve already taken the first step. No matter which card you decide to open next, you’re on the right track! You’ve signed up for our #1 beginner card and snagged one of the best signup offers. Easy cash back is now yours, and you’re well on your way to increasing your bank account. As you decide which card to open next, there are a few things we want you to keep in mind.

Disclaimer: If you decide to open up one of these cards, we’d love for you to sign up using one of our links on this page. We work hard to bring our app and content to you for free. By using the links on our site to apply for credit cards, you’ll help support the site in a big way.

If you’re anything like me when I hit my first signup bonus, you’re probably already contemplating which card you’ll open next. You have a few routes you could take, and we’ve separated the information out by the various situations in which you might find yourself.

Don’t have time to read the whole post? We’ll break down your options below, but the best option for most people is the Citi Strata Premier® Card. The card is easy to earn and redeem points, especially when it comes to cash back. I think this is one of the most underrated rewards cards out there.

Formerly the Citi Premier® Card, this is a new excellent rewards credit card with a solid signup bonus and 3x spending categories. Read the application rule carefully regarding "48 months."

If You Have a Partner

If you have a significant other who does not have their own Chase Sapphire Preferred, this is definitely the first next step to take. Couples have separate credit profiles, so each person can get a primary card to double up on the bonus. Not only is it super valuable for each of you to earn the sign-up bonus for one of the best beginner cards out there, but you can also combine your points together for even more cash back!

If you’re hesitant to pay the annual fee for two of the same cards, it’s important to note that you can easily close or downgrade one of these cards after a year. Paired with the many perks Chase provides for account holders, you might find that this card is well worth the annual fee (even for two people)!

Quick tip: There’s no need to worry if your partner is listed as an Authorized User on your card. They can still open up a card for themselves—making this a huge win!

Last Chance! Offer ends 7/30/26 at 9am ET. Highest-ever limited time offer on our #1 recommended personal card. Hands down the single best “starter card” for beginners and the MVP card for free travel.

If You Have a Small Business

An easy next step for those who have just opened a Chase Sapphire Card is to move onto one of the three Ink Business Cards offered by Chase. They each boast a hefty sign-up bonus and are extremely valuable when looking to redeem your points for cash back. Each of these cards has its own perks, but we recommend the Ink Business Unlimited because of its generous sign-up bonus and simple earning structure.

The #1 reason to get an Ink business card after your Chase Sapphire Preferred is because the welcome offer is generous — especially if you are looking for a no annual fee card. Additionally, keeping your accounts simple with just one bank — that being Chase — helps streamline your credit cards. And, if the time comes where you decide you want to instead redeem your points for travel — instead of cash back — having everything in one “bucket” will help.

Extra Tip: Plus, getting a business card next will allow for even more space between your personal applications when it comes time to get your next personal card.

Highest-ever offer on a top business card, and an easy one to recommend. Great for carrying a balance, if you need to carry a balance. Earn unlimited 1.5% cash back on all purchases.

Highest ever welcome bonus for a standout business card with no annual fee. Great for carrying a balance, if you need to carry a balance.

A highly recommended business card for its signup bonus and 3x (3% cash back) categories on the first $150,000 spent in combined purchases. All Ink cards earn Ultimate Rewards with the option of converting to cash back.

Contrary to popular belief, you don’t have to have a big business in order to qualify for a business credit card. In fact, sole proprietors can apply for business credit cards without any official business registration. Check out our blog post, “Am I Eligible For a Business Credit Card?” to read more about eligibility and learn how to apply for a Chase Ink card as a sole proprietor.

Advanced Tip: Business cards do not impact your 5/24 status (as with most other business cards). However, you do need to be under 5/24 in order to be approved for these cards. Read more below about the Chase “5/24 rule.”

If You Want to Keep Things Completely Simple

If you don’t have a small business, the Citi Strata Premier is a top contender for the next card you should get. This card is consistently one of our highest-rated cards for beginners, and for good reason! Most notably, this card is essentially Citi’s version of the Chase Sapphire Preferred card and has a great signup bonus that is best used when transferring to one of Citi’s transfer partners, or when redeemed as cash back for travel expenses. The value of your points in the portal is the same as cash back (at 1 cent per point), so if you prefer to book directly with an airline or hotel, this is definitely a sweet card for you.

This simple rewards card is also a good option for those whose spouse or travel companion isn’t as involved in credit cards or rewards as you are (we’ve all been there)! Check out this post to learn more about the Citi Premier card and why we love it!

Formerly the Citi Premier® Card, this is a new excellent rewards credit card with a solid signup bonus and 3x spending categories. Read the application rule carefully regarding "48 months."

If you already have the Citi Strata Premier card, The Capital One Venture Rewards Credit Card has earned a top stop as well. Although this is advertised as a ‘travel’ credit card, you can also redeem your Venture miles earned towards cash back. It’s also one of those cards where you don’t need to worry about category spending as you earn the same 2x points for every purchase you make. When used for your everyday spending, your points can quickly add up!

As you may have noticed, there are many rewards credit cards out there that offer incredible value and perks. With so many options out there, it can quickly become overwhelming. Generally speaking, the Capital One Venture Rewards card is a great complement to the Chase Sapphire cards and provides incredible value with its welcome offer and earning potential on everyday purchases.

With this card, you can redeem your miles for cash back at a rate of 0.5 cent per mile. (Note: This is the exact same rate as redeeming your miles earned for gift cards, so we’d recommend cash over a gift card). You have the option to deposit your cash back into your checking or savings account, or you can receive a check by mail. Alternatively, you can also set it up so you’ll receive an automatic cash redemption after reaching a certain mileage threshold. This allows you to fully ‘set and forget’ and your cash back will just start rolling in.

However, this card is probably best known for its ability to use the card for travel purchases and then use miles to erase those charges. This feature allows you to use accumulated miles to offset the cost of eligible travel purchases made with this card. Essentially, you can reimburse yourself for travel expenses.

Now, even if you aren’t traveling, you might be surprised to see what qualifies as travel. Look at your current credit card statement and anything that says ‘travel’ qualifies. This can include Uber rides, the subway and even more of your everyday life.

Zac loves to use points from his Capital One Venture Card to reimburse expenses on his trips, like rental cars, AirBnB’s, hotel bills, and food expenses. His accumulated “miles” helped him offset the costs of these expenses on his trip to Costa Rica, Mexico, and Peru! This means he doesn’t have to worry about hotel and airline availability — a daunting thought to many when thinking about “points and miles”

Best "easy to use" starter card (or complement to the Chase Sapphire Preferred® Credit Card) for those who don't want to think when it comes to earning and redeeming miles.

If You Want to Stick with Chase (and don’t want to open many cards)

If you don’t see yourself opening many cards, but want to maximize your Chase Ultimate Rewards points, you might consider the Chase Freedom® Unlimited or Chase Freedom Flex®. For those who aren’t interested in opening several cards, using one of these cards for earning on everyday purchases could be an ideal addition to your wallet.

While these cards don’t offer huge sign-up bonuses, these no-annual fee options have very straightforward earning structures and allow you to easily redeem your points for cash back — or move your points to your Sapphire Preferred card at a future time for travel redemptions.

With this card, you typically earn 3% cash back on dining (including takeout and select delivery services), 3% cash back on drugstores, 5% cash back on travel purchased through Chase Travel℠, and 1.5% cash back on everything else.

A very strong card that is super flexible for cash back or free travel. Lots of good spending categories and the ability to move points to a premium Chase Ultimate Rewards® card makes this a great card to have.

Things to Keep in Mind

Strategy is Key

If you’re ready to open a new card, it’s important to have a strategy in mind. After all, you want your next card to count as much as the Chase Sapphire Preferred. It’s best to wait 90 days between opening cards, but there are a few exceptions to this rule (especially if you own a business). CashFreely members can use their app to track when it has been 90 days since they last opened a card.

The 5/24 Rule

If you’re new to rewards credit cards, you may not be familiar with Chase’s 5/24 rule. Simply put, Chase will deny your application if you’ve opened 5 or more personal cards in the last 24 months. So, if you’re in this for the long haul, you’ll want to prioritize Chase cards over other card issuers. As a reminder, business cards do not count towards your 5/24 status (with the exception of CapitalOne, TD Bank, and Discover). You can check your 5/24 status, here!

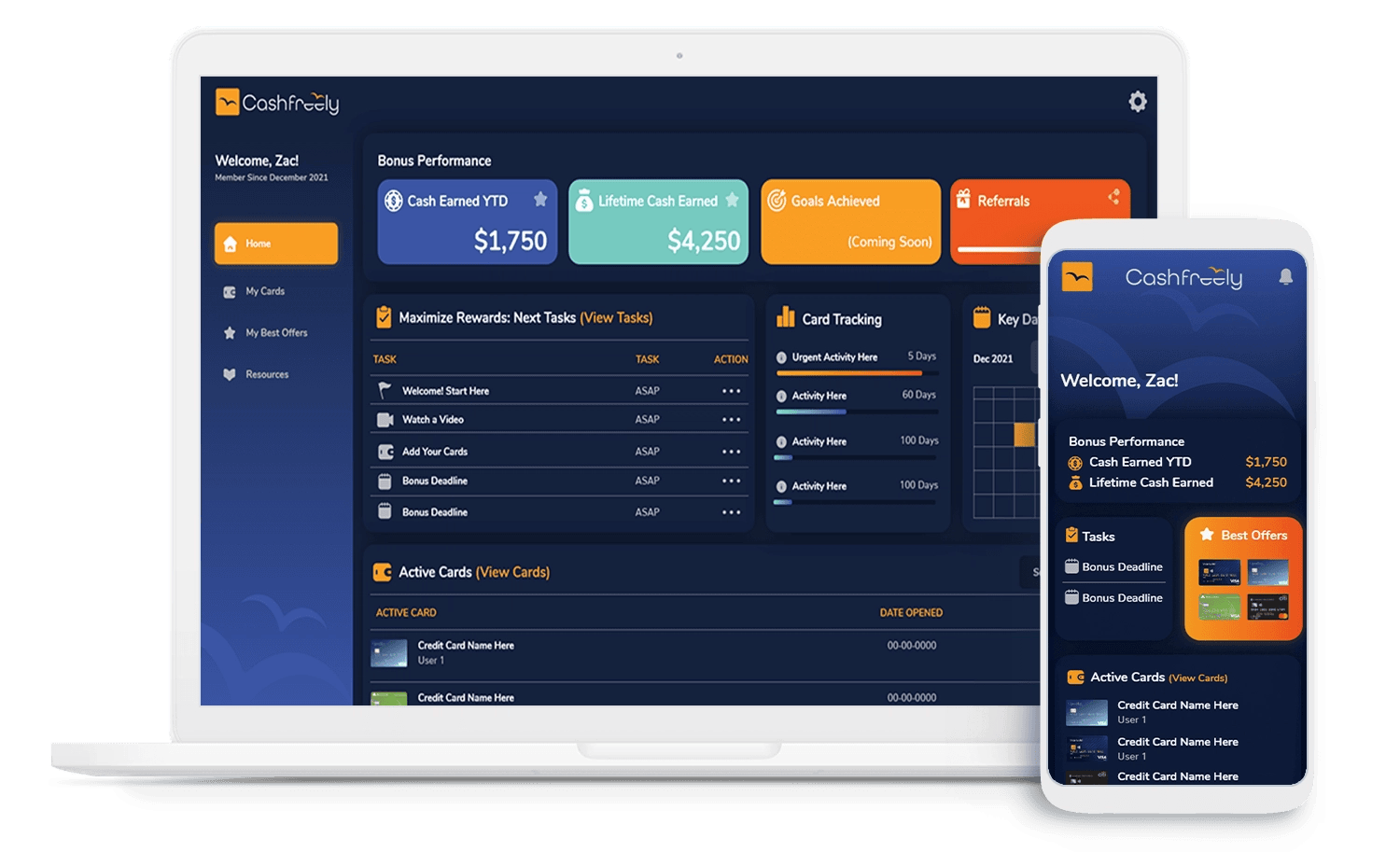

The CashFreely App Can Help You Stay Organized

A common concern with opening many cards is that keeping track of annual fees, 5/24 status, spending categories, and on-time payments can seem daunting. With the CashFreely app, you receive automated reminders for bonus deadlines, annual fees and track your 5/24 status. Even more, you can keep track of the cards for both you and another person!

Don’t see a card in this post that you like? The My Best Offers feature in the CashFreely app will make card recommendations for you based on your 5/24 status and the cards you currently have open.

Summary

You have many choices when it comes to your next step, and earning your bonus on a Chase Sapphire card is just the beginning. It’s exciting to see your points accumulate and help pay for a trip for which you’d otherwise have to break the bank. Sign up for your next card, and be well on your way to earning more cash back.

Cards listed in this post:

Chase Ink Business Unlimited; Chase Ink Business Cash; Chase Ink Business Preferred